Crypto is quietly embedding itself into mainstream American finance. This week, Fannie Mae accepted the first crypto-backed mortgage product in U.S. history, the CLARITY Act inches closer to a Senate vote, and Bitcoin trades at $66,453 in an environment of extreme fear. Beneath the bearish sentiment, structural shifts are accelerating.

TLDR Keypoints

- The CLARITY Act passed the House 294–134 and is now pending Senate action, with Treasury Secretary Bessent targeting a spring 2026 signing.

- Bitcoin trades at $66,453, down roughly 47% from its October 2025 all-time high of $126,080, while the Fear & Greed Index sits at 8 (Extreme Fear).

- Fannie Mae accepted the first crypto-backed mortgage product on March 26, 2026, via a Coinbase and Better Home and Finance partnership.

CLARITY Act Moves Forward: What the Bill Actually Does

The Digital Asset Market Clarity Act of 2025, known as the CLARITY Act (H.R. 3633), passed the U.S. House of Representatives with a bipartisan vote of 294–134 in July 2025. The bill is now pending in the Senate, where it has stalled partly over disagreements about whether unregulated stablecoins should be permitted to offer yield.

At its core, the CLARITY Act draws a jurisdictional line the crypto industry has sought since 2021. The CFTC would gain exclusive jurisdiction over digital commodity spot markets, while the SEC retains authority over investment contract assets. For exchanges, token issuers, and DeFi projects, this distinction determines which regulator they answer to and which compliance framework applies.

Treasury Secretary Scott Bessent has named spring 2026 as the target window for a presidential signing. According to unconfirmed reports, prediction markets price the odds of a 2026 signing at 72%. However, the path forward is not guaranteed. Secondary sources and social media accounts have reported that Coinbase publicly withdrew its support for the current Senate text, arguing it could hamper innovation, weaken competition, and restrict features like stablecoin rewards, though no direct Senate press release has confirmed the committee markup postponement.

If signed into law, the CLARITY Act would represent the most significant piece of U.S. crypto legislation to date. JPMorgan analysts have described the bill as a potential catalyst for institutional Bitcoin adoption, noting that regulatory clarity could be the ultimate spark for the next wave of institutional capital. For context, Ethereum whale activity has been picking up even before the bill’s passage, with large deposits hitting exchanges in recent weeks.

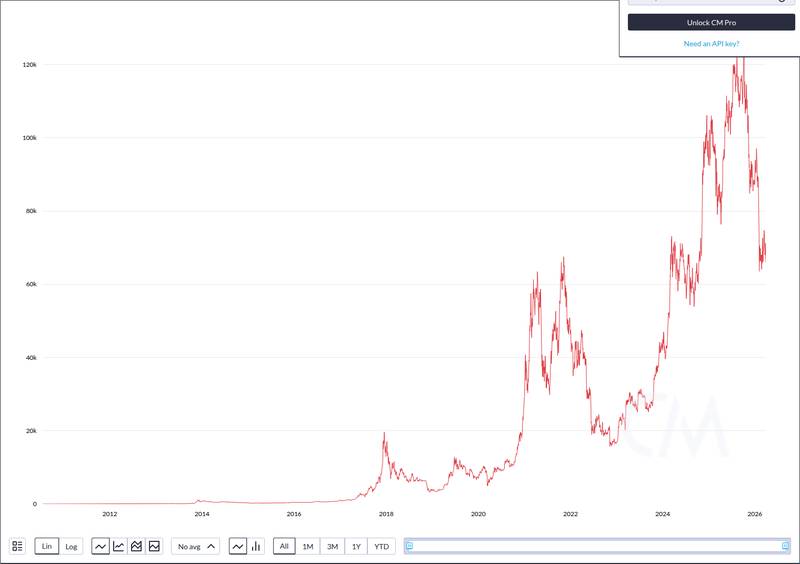

Bitcoin’s Week: Extreme Fear Meets Structural Tailwinds

Bitcoin closed the week trading at approximately $66,453, with a market cap of $1.33 trillion and 24-hour trading volume of $27.06 billion. The price represents a decline of roughly 47% from Bitcoin’s all-time high of $126,080, reached on October 6, 2025.

The Crypto Fear & Greed Index stands at 8 out of 100, labeled “Extreme Fear.” The macro backdrop is weighing heavily on crypto risk appetite: Iran war escalation and a global equity selloff have pushed investors away from risk assets across the board.

Yet beneath the fear, structural catalysts are stacking up. The CLARITY Act’s legislative momentum, the Fannie Mae crypto mortgage milestone, and sustained institutional interest suggest the market may not yet be pricing in regulatory and adoption tailwinds. Bitcoin longs on Bitfinex recently hit 79,343, the highest level since November 2023, signaling that leveraged traders are positioning for a recovery.

The disconnect between extreme sentiment readings and accelerating institutional infrastructure is worth watching. Previous Extreme Fear readings below 10 have historically preceded sharp reversals, though past patterns are not guarantees.

Crypto-Backed Mortgages: DeFi Meets Real Estate

On March 26, 2026, Fannie Mae accepted the first crypto-backed mortgage product in U.S. history, launched through a partnership between Better Home and Finance and Coinbase. The product allows borrowers to pledge Bitcoin or USDC as collateral for a second loan that funds the down payment on a primary Fannie Mae-backed mortgage.

The mechanics work like this: on a $500,000 home, a borrower can pledge $250,000 in Bitcoin and receive a $100,000 loan to cover the cash down payment. The crypto assets remain in custody in Better’s Coinbase Prime account for the life of the loan and cannot be traded. Collateral is only at risk of liquidation after a 60-day payment delinquency.

Rates on crypto-backed mortgages run 0.5 to 1.5 percentage points higher than standard 30-year loans. Coinbase One members are eligible for a 1% rebate on the mortgage value, capped at $10,000. While the product currently supports Bitcoin and USDC, other assets like Ethereum and Solana may be added in the future.

“We have now finally created the infrastructure rails to enable any tokenized asset in America to be able to be pledged to help someone afford to buy a home. It starts with bitcoin, starts with [USD Coin], but going forward, it can be Apple stock or Amazon stock, or any publicly traded mutual fund, bond fund, something that you might hold in your IRA, you’re going to be able to pledge that to buy a home.”

— Vishal Garg, CEO, Better Home and Finance

Max Branzburg, Head of Consumer and Business Products at Coinbase, described token-backed mortgages as “a major first step to unlocking homeownership for the younger generations that have struggled with barriers to saving for a traditional down payment.”

The demographic case supports this. Gen Z and Millennials hold approximately 25% of their portfolios in non-traditional assets like crypto, and 73% say it is harder to build wealth by traditional means. For younger buyers already holding significant crypto positions, the ability to leverage those holdings for a down payment without selling, and triggering a taxable event, fills a real gap. Meanwhile, the broader DeFi-to-real-world pipeline continues to develop, as protocols like Lido launch new yield products that bridge on-chain assets and traditional finance.

The Federal Housing Finance Agency, Fannie Mae’s conservator, has been increasingly open to cryptocurrency. Combined with the CLARITY Act’s potential to provide regulatory certainty, the crypto mortgage launch suggests that digital assets are moving from speculative instruments to foundational components of American financial infrastructure, even as the market itself sits in extreme fear.

Disclaimer: This article is for informational purposes only and does not constitute financial or investment advice. Cryptocurrency and digital asset markets carry significant risk. Always do your own research before making decisions.