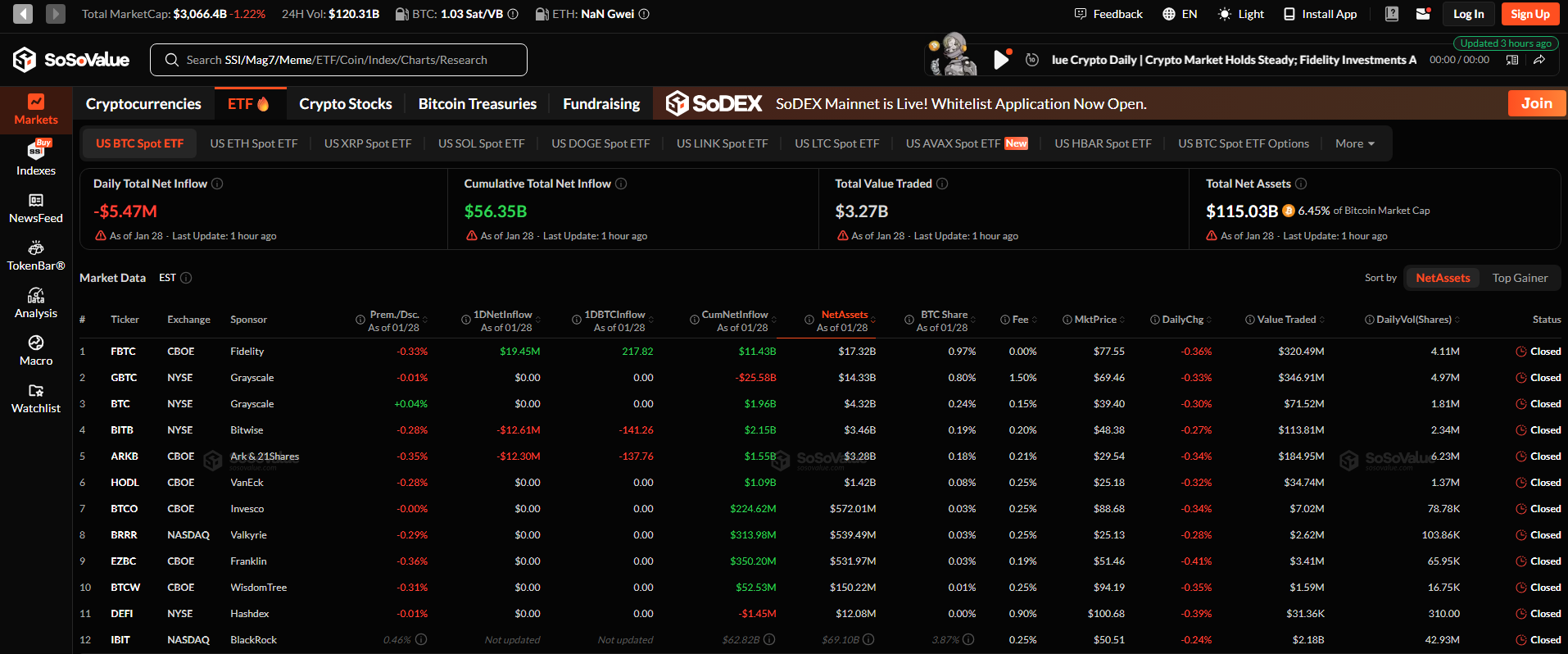

BlackRock has filed a preliminary Form S-1 with the U.S. Securities and Exchange Commission to launch the iShares Bitcoin Premium Income ETF, an options-based Bitcoin fund that aims to generate yield from IBIT call options.

The filing signals BlackRock’s expansion of Bitcoin ETFs from pure price tracking into yield-generating investment products, reflecting growing demand for income-oriented crypto exposure.

By introducing a covered-call strategy on IBIT, BlackRock is positioning Bitcoin as a volatility-harvesting asset rather than just a speculative one, even though investors must accept capped upside, residual downside risk, and higher costs compared with holding a spot Bitcoin ETF directly.

What BlackRock filed: iShares Bitcoin Premium Income ETF, U.S. SEC status

BlackRock has filed a preliminary S-1 with the U.S. SEC for the iShares Bitcoin Premium Income ETF, but the fund is not yet approved and has not started trading.

The filing was submitted on January 23, 2026 and is currently under SEC review, which typically takes months and may involve amendments before approval is granted.

The ETF is designed to give investors Bitcoin price exposure plus income by running a covered-call strategy on BlackRock’s existing iShares Bitcoin Trust (IBIT).

Key regulatory facts:

- Status: Preliminary S-1, not approved

- Trading: Not live on any exchange

- Ticker and fee: Not yet disclosed

- Structure: Holds Bitcoin and sells options on IBIT

This filing formally turns Bitcoin into an income-producing ETF category inside U.S. securities law, not a crypto product.

How IBIT covered calls earn options premium: strike price, roll cadence

The ETF earns income by selling call options on IBIT shares and collecting the option premiums as cash. This is a covered-call strategy in which BlackRock sells the right for someone else to buy IBIT at a higher price in exchange for immediate income.

The process works as follows:

- The fund holds IBIT, which holds spot Bitcoin

- It sells out-of-the-money call options on IBIT

- Buyers pay a premium

- That premium becomes ETF income

Strike prices are set above the current IBIT price, and the options are rolled continuously through active management rather than a fixed monthly schedule. Higher Bitcoin volatility means higher option premiums, which directly raises the ETF’s yield.

Trade-offs and risks: capped BTC upside, residual downside, tracking, liquidity, volatility

The ETF sacrifices Bitcoin’s upside in bull markets while still remaining exposed to most downside risk. Because it sells call options, the fund must give up gains above the strike price when Bitcoin rallies, but it still loses value when Bitcoin falls

| Risk | What it means |

|---|---|

| Capped upside | If Bitcoin rallies above the call strike, the ETF must sell IBIT at that lower price, missing further gains |

| Residual downside | The option premium only gives a small buffer. If BTC crashes, the ETF still falls with it |

| Tracking | Returns will differ from spot Bitcoin because income replaces price exposure |

| Liquidity | Depends on both IBIT’s options market and the ETF’s own trading volume |

| Volatility | High volatility creates income but also raises the chance of losses and forced option assignment |

This ETF is structurally designed to underperform IBIT in strong bull markets but to provide steadier cash flow when Bitcoin trades sideways.

Costs and ownership: expense ratio, spreads, volume, NAV behavior

Expense ratio, bid-ask spread, trading volume, and NAV drive total cost

The true cost of owning BlackRock’s Bitcoin Premium Income ETF comes from its management fee, bid-ask spreads, trading liquidity, and how option payouts affect NAV.

Although BlackRock has not yet disclosed the expense ratio, covered-call ETFs typically charge three to four times more than spot Bitcoin ETFs because they require continuous option trading and portfolio management.

In practice, investors pay through four layers:

- Expense ratio: IBIT charges about 0.25 percent. Covered-call ETFs usually charge close to 1 percent because of options execution, compliance, and active management.

- Bid-ask spread: A new ETF normally trades with wider spreads than IBIT. That means investors lose value when entering and exiting positions.

- Trading volume: Higher volume tightens spreads and improves price discovery. Until the ETF scales, execution costs will be higher than IBIT.

- NAV behavior: Because the fund distributes option income, its net asset value does not compound the same way as Bitcoin. Paying out premiums means NAV grows slower and can even decline in flat markets.

Tracking error and liquidity versus spot Bitcoin ETF, futures-based options

The ETF will not track Bitcoin as closely as IBIT because selling call options permanently alters its return profile. IBIT reflects spot Bitcoin price movements, while this fund gives up upside above the strike price.

Liquidity will be better than futures-based Bitcoin ETFs but weaker than IBIT itself. The fund benefits from IBIT’s deep options and share liquidity, but its own trading volume will still determine spreads and execution quality. Until it scales, liquidity costs will remain higher than IBIT.

Futures-based Bitcoin ETFs lose value through contract roll and contango, while this ETF avoids those issues. Instead, it sacrifices returns through option overwriting when Bitcoin prices move sharply upward. The cost is paid in foregone upside rather than futures decay.

Distributions and taxes: schedule, variability, 1099 reporting, potential return of capital

Distribution yield mechanics, schedule variability, potential return of capital (ROC)

Distributions come from selling call options on IBIT rather than from selling Bitcoin itself. When Bitcoin volatility is high, option premiums rise and ETF income increases. When volatility falls, payouts decline even if Bitcoin prices remain elevated.

Monthly income will fluctuate because Bitcoin’s volatility changes constantly. This ETF does not provide a fixed yield like bonds or money market funds. Its income is entirely dependent on how much traders are willing to pay for Bitcoin upside through options.

A significant portion of distributions may be classified as return of capital rather than true investment profit. Return of capital means part of the investor’s own money is being returned. This reduces the cost basis of ETF shares and increases taxable gains when they are eventually sold.

1099 tax reporting for call options premium and distributions

Investors will receive Form 1099-DIV and 1099-B instead of crypto tax reports. Investors receive brokerage tax forms instead of blockchain transaction records. This allows the ETF to be held in retirement accounts and traditional portfolios.

Option premium income is typically taxed as ordinary income, while return of capital is tax deferred. The 1099-DIV separates these categories so investors can see exactly how each distribution is classified. This determines when and how taxes are owed.

Capital gains are calculated when ETF shares are sold using the adjusted cost basis after return of capital. As ROC lowers the cost basis over time, a larger portion of the sale price becomes taxable. This makes tax planning important for long-term holders of the ETF.

| Disclaimer: This website provides information only and is not financial advice. Cryptocurrency investments are risky. We do not guarantee accuracy and are not liable for losses. Conduct your own research before investing. |